10. How to Pay for a War: Part 2#

10.1. Overview#

This lecture presents another application of Markov jump linear quadratic dynamic programming and constitutes a sequel to an earlier lecture.

We use a method introduced in lecture Markov Jump LQ dynamic programming toimplement suggestions by [Barro, 1999] and [Barro and McCleary, 2003]) for extending his classic 1979 model of tax smoothing.

[Barro, 1979] model is about a government that borrows and lends in order to help it minimize an intertemporal measure of distortions caused by taxes.

Technically, [Barro, 1979] model looks a lot like a consumption-smoothing model.

Our generalizations of [Barro, 1979] will also look like souped-up consumption-smoothing models.

Wanting tractability induced [Barro, 1979] to assume that

the government trades only one-period risk-free debt, and

the one-period risk-free interest rate is constant

In our earlier lecture, we relaxed the second of these assumptions but not the first.

In particular, we used Markov jump linear quadratic dynamic programming to allow the exogenous interest rate to vary over time.

In this lecture, we add a maturity composition decision to the government’s problem by expanding the dimension of the state.

We assume

that the government borrows or saves in the form of risk-free bonds of maturities

that interest rates on those bonds are time-varying and in particular are governed by a jointly stationary stochastic process.

In addition to what’s in Anaconda, this lecture deploys the quantecon library:

!pip install --upgrade quantecon

Let’s start with some standard imports:

import quantecon as qe

import numpy as np

import matplotlib.pyplot as plt

10.2. Two example specifications#

We’ll describe two possible specifications

In one, each period the government issues zero-coupon bonds of one- and two-period maturities and redeems them only when they mature – in this version, the maturity structure of government debt at each date is partly inherited from the past.

In the second, the government redesigns the maturity structure of the debt each period.

10.3. One- and Two-period Bonds but No Restructuring#

Let

Evidently,

In the spirit of [Barro, 1979], government expenditures are governed by an exogenous stochastic process.

Given initial conditions

subject to the constraints

Here

variables

The parameter

This penalty deters the government from taking large “long-short” positions in debt of different maturities.

An example below will show the penalty in action.

As well as extending the model to allow for a maturity decision for

government debt, we can also in principle allow the matrices

Below, we will often adopt the convention that for matrices appearing in a linear state space,

10.4. Mapping into an LQ Markov Jump Problem#

First, define

which is debt due at time

Then define the endogenous part of the state:

and the complete state vector

and the control vector

The endogenous part of state vector follows the law of motion:

or

Define the following functions of the state

and

where

Define

Note that in discrete Markov state

It follows that

or

where

Because the payoff function also includes the penalty parameter on issuing debt of different maturities, we have:

where

Therefore, the appropriate

The law of motion of the state in all discrete Markov states

where

Thus, in this problem all the matrices apart from

As shown in the previous lecture, when provided with appropriate

LQMarkov class can solve Markov jump LQ problems.

The function below maps the primitive matrices and parameters from the above

two-period model into the matrices that the LQMarkov class requires:

def LQ_markov_mapping(A22, C2, Ug, p1, p2, c1=0):

"""

Function which takes A22, C2, Ug, p_{t, t+1}, p_{t, t+2} and penalty

parameter c1, and returns the required matrices for the LQMarkov

model: A, B, C, R, Q, W.

This version uses the condensed version of the endogenous state.

"""

# Make sure all matrices can be treated as 2D arrays

A22 = np.atleast_2d(A22)

C2 = np.atleast_2d(C2)

Ug = np.atleast_2d(Ug)

p1 = np.atleast_2d(p1)

p2 = np.atleast_2d(p2)

# Find the number of states (z) and shocks (w)

nz, nw = C2.shape

# Create A11, B1, S1, S2, Sg, S matrices

A11 = np.zeros((2, 2))

A11[0, 1] = 1

B1 = np.eye(2)

S1 = np.hstack((np.eye(1), np.zeros((1, nz+1))))

Sg = np.hstack((np.zeros((1, 2)), Ug))

S = S1 + Sg

# Create M matrix

M = np.hstack((-p1, -p2))

# Create A, B, C matrices

A_T = np.hstack((A11, np.zeros((2, nz))))

A_B = np.hstack((np.zeros((nz, 2)), A22))

A = np.vstack((A_T, A_B))

B = np.vstack((B1, np.zeros((nz, 2))))

C = np.vstack((np.zeros((2, nw)), C2))

# Create Q^c matrix

Qc = np.array([[1, -1], [-1, 1]])

# Create R, Q, W matrices

R = S.T @ S

Q = M.T @ M + c1 * Qc

W = M.T @ S

return A, B, C, R, Q, W

With the above function, we can proceed to solve the model in two steps:

Use

LQ_markov_mappingto mapUse the

LQMarkovclass to solve the resulting n-state Markov jump LQ problem.

10.5. Penalty on Different Issues Across Maturities#

To implement a simple example of the two-period model, we assume that

To do this, we set

Therefore, in this example,

We will assume that there are two Markov states, one with a flatter yield curve, and one with a steeper yield curve.

In state 1, prices are:

and in state 2, prices are:

We first solve the model with no penalty parameter on different issuance

across maturities, i.e.

We specify that the transition matrix for the Markov state is

Thus, each Markov state is persistent, and there is an equal chance of moving from one to the other.

# Model parameters

β, Gbar, ρ, σ, c1 = 0.95, 5, 0.8, 1, 0

p1, p2, p3, p4 = β, β**2 - 0.02, β, β**2 + 0.02

# Basic model matrices

A22 = np.array([[1, 0], [Gbar, ρ] ,])

C_2 = np.array([[0], [σ]])

Ug = np.array([[0, 1]])

A1, B1, C1, R1, Q1, W1 = LQ_markov_mapping(A22, C_2, Ug, p1, p2, c1)

A2, B2, C2, R2, Q2, W2 = LQ_markov_mapping(A22, C_2, Ug, p3, p4, c1)

# Small penalties on debt required to implement no-Ponzi scheme

R1[0, 0] = R1[0, 0] + 1e-9

R2[0, 0] = R2[0, 0] + 1e-9

# Construct lists of matrices correspond to each state

As = [A1, A2]

Bs = [B1, B2]

Cs = [C1, C2]

Rs = [R1, R2]

Qs = [Q1, Q2]

Ws = [W1, W2]

Π = np.array([[0.9, 0.1],

[0.1, 0.9]])

# Construct and solve the model using the LQMarkov class

lqm = qe.LQMarkov(Π, Qs, Rs, As, Bs, Cs=Cs, Ns=Ws, beta=β)

lqm.stationary_values()

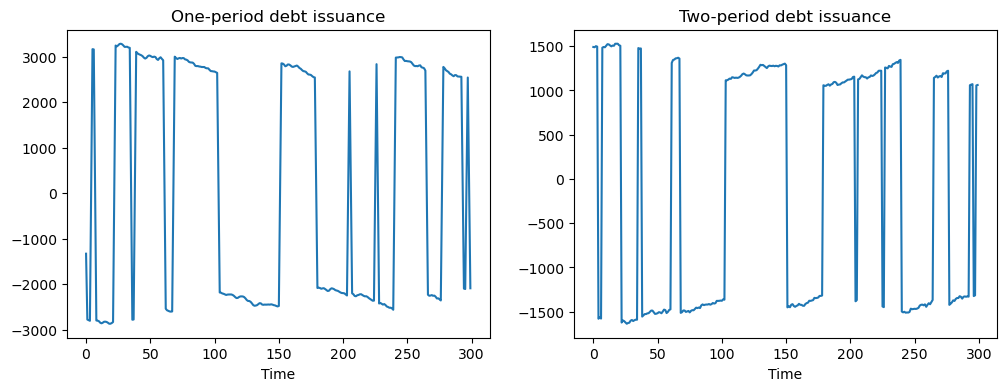

# Simulate the model

x0 = np.array([[100, 50, 1, 10]])

x, u, w, t = lqm.compute_sequence(x0, ts_length=300)

# Plot of one and two-period debt issuance

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(12, 4))

ax1.plot(u[0, :])

ax1.set_title('One-period debt issuance')

ax1.set_xlabel('Time')

ax2.plot(u[1, :])

ax2.set_title('Two-period debt issuance')

ax2.set_xlabel('Time')

plt.show()

The above simulations show that when no penalty is imposed on different issuances across maturities, the government has an incentive to take large “long-short” positions in debt of different maturities.

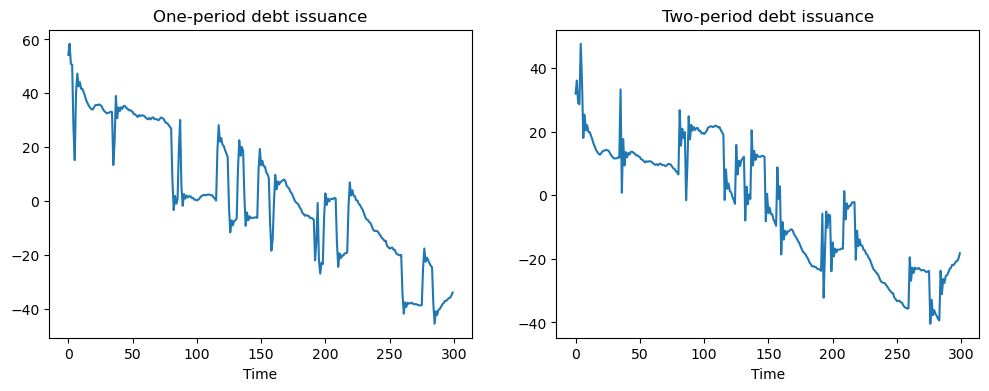

To prevent such outcomes, we set

This penalty is big enough to motivate the government to issue positive quantities of both one- and two-period debt:

# Put small penalty on different issuance across maturities

c1 = 0.01

A1, B1, C1, R1, Q1, W1 = LQ_markov_mapping(A22, C_2, Ug, p1, p2, c1)

A2, B2, C2, R2, Q2, W2 = LQ_markov_mapping(A22, C_2, Ug, p3, p4, c1)

# Small penalties on debt required to implement no-Ponzi scheme

R1[0, 0] = R1[0, 0] + 1e-9

R2[0, 0] = R2[0, 0] + 1e-9

# Construct lists of matrices

As = [A1, A2]

Bs = [B1, B2]

Cs = [C1, C2]

Rs = [R1, R2]

Qs = [Q1, Q2]

Ws = [W1, W2]

# Construct and solve the model using the LQMarkov class

lqm2 = qe.LQMarkov(Π, Qs, Rs, As, Bs, Cs=Cs, Ns=Ws, beta=β)

lqm2.stationary_values()

# Simulate the model

x, u, w, t = lqm2.compute_sequence(x0, ts_length=300)

# Plot of one and two-period debt issuance

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(12, 4))

ax1.plot(u[0, :])

ax1.set_title('One-period debt issuance')

ax1.set_xlabel('Time')

ax2.plot(u[1, :])

ax2.set_title('Two-period debt issuance')

ax2.set_xlabel('Time')

plt.show()

10.6. A Model with Restructuring#

We now alter two features of the previous model:

The maximum horizon of government debt is now extended to a general H periods.

The government is able to redesign the maturity structure of debt every period.

We impose a cost on adjusting issuance of each maturity by amending the payoff function to become:

The government’s budget constraint is now:

To map this into the Markov Jump LQ framework, we define state and control variables.

Let:

Thus,

As before, we will

also have the exogenous state

Therefore, the full state is:

We also define a vector

Finally, we define three useful matrices

In terms of dimensions, the first two matrices defined above are

The last is

We can now write the government’s budget constraint in matrix notation.

We can rearrange the government budget constraint to become

or

To express

To simplify the notation, let

Then

Therefore

where

where to economize on notation we adopt the convention that for the linear state matrices

We’ll use this convention for the linear state matrices

Because the payoff function also includes the penalty parameter for rescheduling, we have:

Because the complete state is

where

Multiplying this out gives:

Therefore, with the cost term, we must amend our

To finish mapping into the Markov jump LQ setup, we need to construct the law of motion for the full state.

This is simpler than in the

previous setup, as we now have

Therefore:

where

This completes the mapping into a Markov jump LQ problem.

10.7. Restructuring as a Markov Jump Linear Quadratic Control Problem#

We can define a function that maps the primitives

of the model with restructuring into the matrices required by the LQMarkov

class:

def LQ_markov_mapping_restruct(A22, C2, Ug, T, p_t, c=0):

"""

Function which takes A22, C2, T, p_t, c and returns the

required matrices for the LQMarkov model: A, B, C, R, Q, W

Note, p_t should be a T by 1 matrix

c is the rescheduling cost (a scalar)

This version uses the condensed version of the endogenous state

"""

# Make sure all matrices can be treated as 2D arrays

A22 = np.atleast_2d(A22)

C2 = np.atleast_2d(C2)

Ug = np.atleast_2d(Ug)

p_t = np.atleast_2d(p_t)

# Find the number of states (z) and shocks (w)

nz, nw = C2.shape

# Create Sx, tSx, Ss, S_t matrices (tSx stands for \tilde S_x)

Ss = np.hstack((np.eye(T-1), np.zeros((T-1, 1))))

Sx = np.hstack((np.zeros((T-1, 1)), np.eye(T-1)))

tSx = np.zeros((1, T))

tSx[0, 0] = 1

S_t = np.hstack((tSx + p_t.T @ Ss.T @ Sx, Ug))

# Create A, B, C matrices

A_T = np.hstack((np.zeros((T, T)), np.zeros((T, nz))))

A_B = np.hstack((np.zeros((nz, T)), A22))

A = np.vstack((A_T, A_B))

B = np.vstack((np.eye(T), np.zeros((nz, T))))

C = np.vstack((np.zeros((T, nw)), C2))

# Create cost matrix Sc

Sc = np.hstack((np.eye(T), np.zeros((T, nz))))

# Create R_t, Q_t, W_t matrices

R_c = S_t.T @ S_t + c * Sc.T @ Sc

Q_c = p_t @ p_t.T + c * np.eye(T)

W_c = -p_t @ S_t - c * Sc

return A, B, C, R_c, Q_c, W_c

10.7.1. Example with Restructuring#

As an example let

Assume that there are two Markov states, one with a flatter yield curve, the other with a steeper yield curve.

In state 1, prices are:

and in state 2, prices are:

We specify the same transition matrix and

# New model parameters

H = 3

p1 = np.array([[0.9695], [0.902], [0.8369]])

p2 = np.array([[0.9295], [0.902], [0.8769]])

Pi = np.array([[0.9, 0.1], [0.1, 0.9]])

# Put penalty on different issuance across maturities

c2 = 0.5

A1, B1, C1, R1, Q1, W1 = LQ_markov_mapping_restruct(A22, C_2, Ug, H, p1, c2)

A2, B2, C2, R2, Q2, W2 = LQ_markov_mapping_restruct(A22, C_2, Ug, H, p2, c2)

# Small penalties on debt required to implement no-Ponzi scheme

R1[0, 0] = R1[0, 0] + 1e-9

R1[1, 1] = R1[1, 1] + 1e-9

R1[2, 2] = R1[2, 2] + 1e-9

R2[0, 0] = R2[0, 0] + 1e-9

R2[1, 1] = R2[1, 1] + 1e-9

R2[2, 2] = R2[2, 2] + 1e-9

# Construct lists of matrices

As = [A1, A2]

Bs = [B1, B2]

Cs = [C1, C2]

Rs = [R1, R2]

Qs = [Q1, Q2]

Ws = [W1, W2]

# Construct and solve the model using the LQMarkov class

lqm3 = qe.LQMarkov(Π, Qs, Rs, As, Bs, Cs=Cs, Ns=Ws, beta=β)

lqm3.stationary_values()

x0 = np.array([[5000, 5000, 5000, 1, 10]])

x, u, w, t = lqm3.compute_sequence(x0, ts_length=300)

# Plots of different maturities debt issuance

fig, (ax1, ax2, ax3, ax4) = plt.subplots(1, 4, figsize=(11, 3))

ax1.plot(u[0, :])

ax1.set_title('One-period debt issuance')

ax1.set_xlabel('Time')

ax2.plot(u[1, :])

ax2.set_title('Two-period debt issuance')

ax2.set_xlabel('Time')

ax3.plot(u[2, :])

ax3.set_title('Three-period debt issuance')

ax3.set_xlabel('Time')

ax4.plot(u[0, :] + u[1, :] + u[2, :])

ax4.set_title('Total debt issuance')

ax4.set_xlabel('Time')

plt.tight_layout()

plt.show()

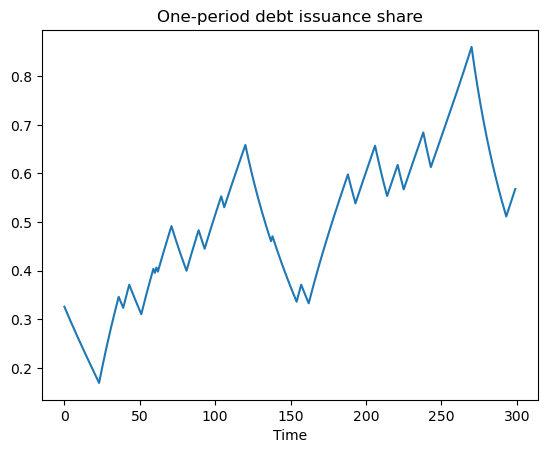

# Plot share of debt issuance that is short-term

fig, ax = plt.subplots()

ax.plot((u[0, :] / (u[0, :] + u[1, :] + u[2, :])))

ax.set_title('One-period debt issuance share')

ax.set_xlabel('Time')

plt.show()